Apr 15, 2025

The equity markets around the world responded to the Trump administration's "Liberation Day" tariff announcement with a three-day sell-off that ranks among the worst in 80 years.

Did we foresee the magnitude of the market's response to the administration's tariff announcement? No, we did not because the tariff announcement exceeded almost anyone's worst-case scenario. For months, we recognized that our equity markets were generally fully priced at best, the large-cap U.S. equity market had a "Magnificent 7" influenced imbalance that was reaching extreme levels, and we held an informed opinion that any material shift by the U.S. to institute protectionist tariffs would be negative for economic growth, inflation, and international relations. Our caution does not mean that we are not long-term optimistic; it simply means that with an equity market that was fully valued at best at the beginning of the year, we anticipated that any significant economic policy changes would introduce heightened uncertainty for the markets to digest.

During the first three months of the year, we responded to what we were expecting in a measured manner in order to reduce equity exposure, add downside-protected securities, add bond exposure, and pair back on or eliminate exposure to the parts of the equity market that were creating the imbalance. In addition, we reduced or eliminated those equities that we believed would be most exposed to the negative aspects of new U.S. tariffs.

Now that we have seen the market's initial response to the April 2nd tariff announcements, we are glad we took a more cautious stance during the first three months of the year. Still, we, along with virtually every economist, business leader, and head of state worldwide, could not have imagined how onerous the initial tariff announcement was. We are unapologetically enthusiastic supporters of free market capitalism as historically practiced in the United States. This view of free-market capitalism has underpinned our enduring optimism about the wisdom of being a long-term investor in our capital markets. We remain hopeful that, when all is said and done, on a net-net basis, global trade barriers will settle in a freer state than they have been over the last 10-20 years.

So, are we still optimistic about the prospect of being long-term investors? The answer to this question is without hesitation, yes! Reflecting on the economic policy announcements of the last several weeks, global trade relationships will be reshaped. Such a reshaping of nearly half a century of global economic order, primarily put in place by the United States, has been a shock to the system for businesses and trading partners worldwide. It is only realistic for markets to react to the disruption of the normal state economic order, and we are experiencing the markets' attempt to sort out the cause and effect of such change without a lot of certainty as to what the new normal state will look like.

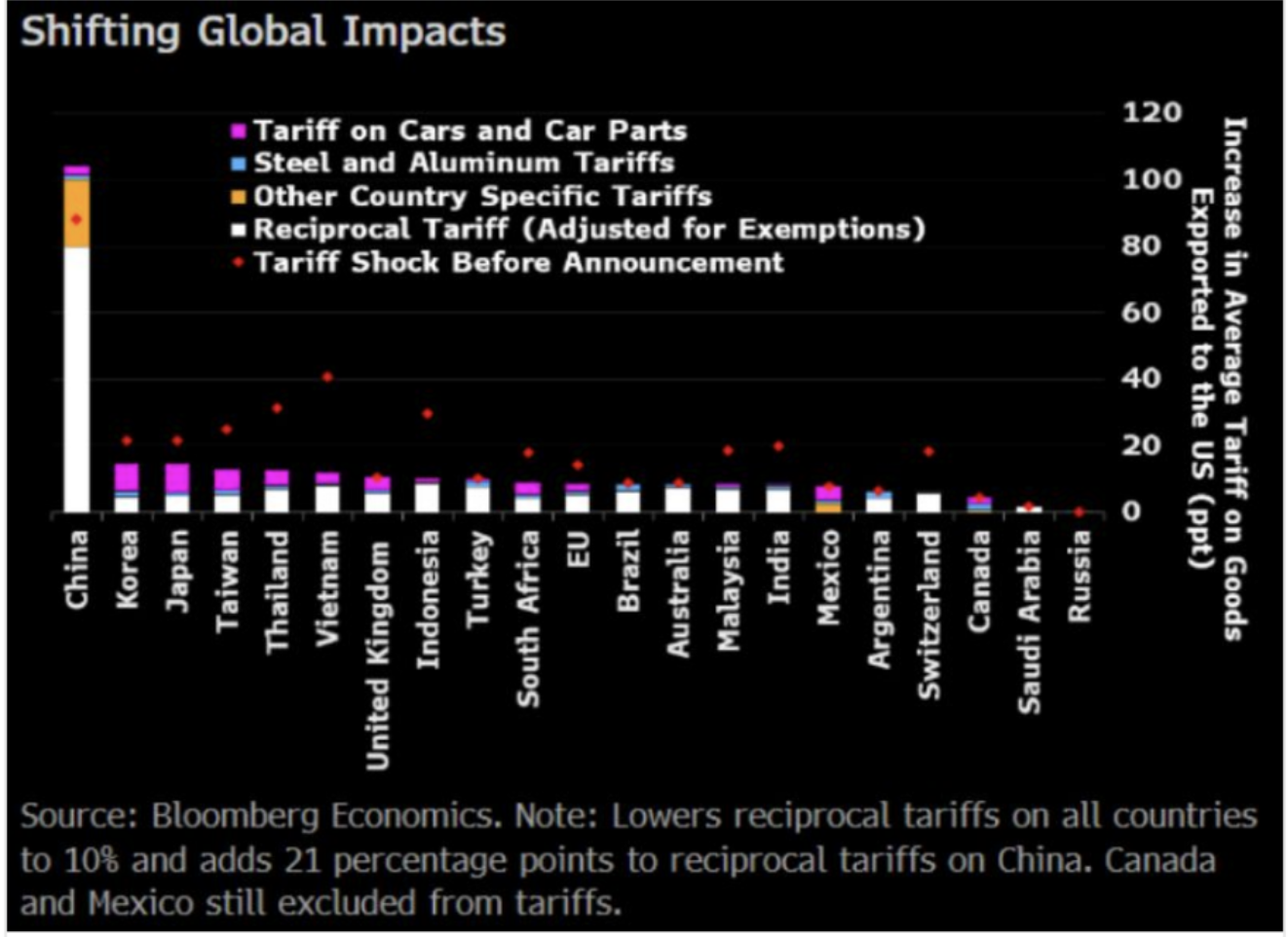

Our base case right now, after the originally announced "reciprocal" tariffs have been paused for 90 days, is that the likelihood that cooler heads will prevail to avoid a tariff scenario that markets were pricing in during the days following the April 2nd announcement has fallen. But, in the meantime, there will be disruption to which markets will continue to react because even with the 90-day pause of the unexpectedly high trade deficit calculated "reciprocal" tariff rates, the weighted average U.S. tariff rate, according to an illustration prepared by Bloomberg Economics, shown below, is still historically high:

Liz Ann Sonders, Chief Investment Strategist of Charles Schwab, posted the illustration above and commented that "Reciprocal tariff of 125% on Chinese goods imports skews rates relative to other countries by a significant degree ... and average effective tariff rate for all imports is still higher than 20%."

Markets are likely to remain highly attuned to economic indicators relating to growth and inflation expectations. We would not be looking for a "V" shaped recovery in equity markets so long as the heightened level of uncertainty remains at the forefront of investors' minds. Of course, events such as the Federal Reserve interjecting significant liquidity into those markets as they did in 2023, following the failure of Silicon Valley Bank, or meaningful actions by policymakers here and around the world to de-escalate the trade wars emerging, would go a long way toward allaying the markets' uncertainty-driven fears.

The markets are caught in the middle of a U.S.-initiated trade war, not against one or two countries but against the entire world. Given this backdrop and the reasons above, we will continue with a heightened cautious posture until stable policy returns and economic fundamentals begin to come into better focus.