After eight months that included a negative GDP reading in the first quarter, a rebound in economic growth in the second quarter, and a third quarter GDP that appears to be tracking at 3%, give or take half a percent. 2025 has also seen inflation measures that are not presenting troublesome upward pressures at the headline level. However, progress in getting headline inflation down to the Federal Reserve's target level of 2% appears to have stalled, with most measures of inflation stuck in the high 2% to low 3% range. Lastly, and possibly the most important factor in the direction of monetary policy, is the employment data. On average, 2025 has seen a meaningful cooling in job creation. Additionally, seasonal revisions have statistically eliminated nearly one million jobs from the previously reported numbers over the last twelve months.

The mosaic of all this information will inform the Federal Reserve Board of Governors in terms of what we get from monetary policy over the balance of the year. The bond and stock markets appear to be discounting a resumption of interest rate cuts beginning this month. The only disagreement within the markets is how aggressively the Federal Reserve will act in terms of resuming cutting their Fed Funds Rate. Already, the interest rate-sensitive industries, such as housing, have seen their constituent stocks rise in anticipation of interest rate relief that theoretically should improve demand in those areas.

However, interest rates may not move as anticipated across the time spectrum of maturities. Federal Reserve interest rates will most definitely move shorter-term market rates, but the effect on longer-term rates that generally directly inform market rates, such as mortgage loan rates, does not necessarily follow shorter-term rates in lock step. In fact, when the Federal Reserve lowered the Fed Funds Rate last fall, longer-term rates rose, confounding many who expected lower longer-term rates.

Shorter-term interest rates are directly informed by monetary policy rate setting; however, long-term market rates, such as the bell-weather 10-Year Treasury Note rate, are a function of both the term premium (time value measure) and long-term inflation expectations. The level of short-term rates can impact the term premium itself, but inflation expectations are what can cause counterintuitive rate direction moves for these longer-term interest rates.

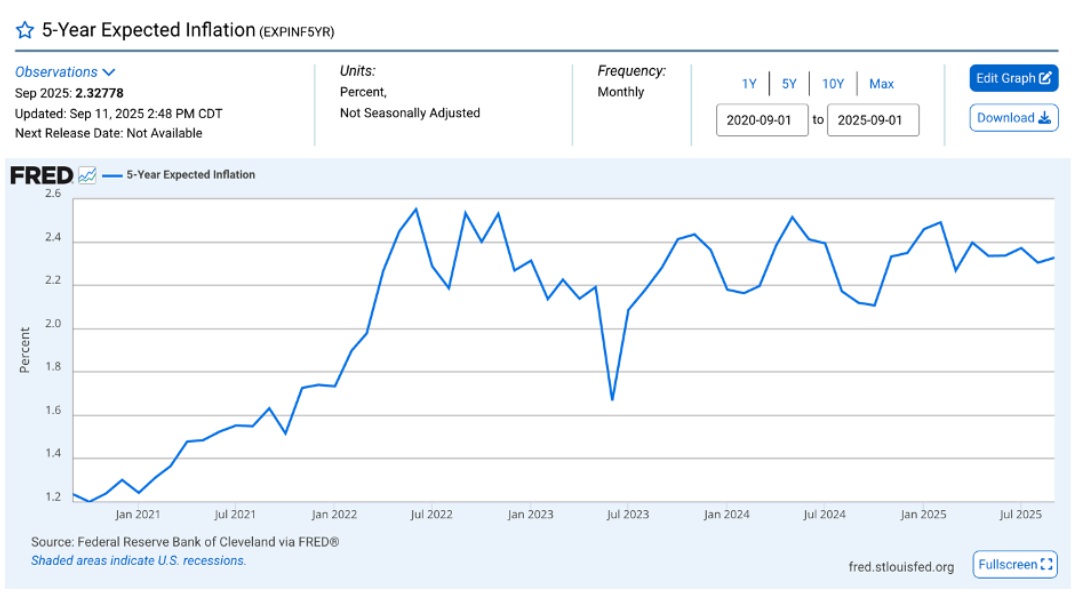

For much of last year, long-term inflation expectations were in decline. Beginning in October, inflation expectations started to move higher, and that trend continued in the first quarter of 2025 and has since leveled out near levels that are near the top of the range of expectations over the last three years. See these inflation expectations in the Federal Reserve Bank of Cleveland chart below:

I am writing this commentary before the September Federal Reserve Open Market Committee meeting this month. I anticipate that the outcome of this month's meeting will be the first rate cut of 2025, and the Federal Reserve Chairman will talk about the balance of risk coming down in favor of supporting the full employment side of their mandate and remaining patient in terms of bringing inflation down to their 2% target. What this means for investors is that the Federal Reserve is likely to resume its series of rate cuts that it began last year to bring the Fed Funds rate down toward what they deem to be the neutral rate. However, this posture can only be maintained if the economy slows without stalling and inflation does not continue to surprise on the upside. Should the economy stall out and flirt with a recession, rate cuts could move the Fed Funds rate below neutral to accommodative, and that would be familiar territory for the Federal Reserve policymakers; however, should the economy stall out with steadily rising inflation, the Federal Reserve would face its most challenging economic environment, stagflation.

A stagflation economy puts the Federal Reserve's Congressional-mandated dual mandate in conflict, meaning the Federal Reserve policymakers find themselves in a "no-win" situation. If they continue to cut rates to support employment, they stimulate economic growth, which most economists agree puts upward pressure on inflation. A stagflation environment will also keep long-term interest rates stubbornly high relative to the Federal Reserve controlled short-term interest rates, commonly referred to as a steepening yield curve.

We are not ready to make stagflation our base forecast for the next 12 to 18 months, but we are pretty sure that the word stagflation will be a highly "trending" economic term over the next year.

For equity investors, a goldilocks environment with respect to economic growth and inflation can be a conducive environment for a continuation of the current bull market. In fact, a "goldilocks" economy that is supportive of rate cuts should stimulate a broadening effect within the equity markets. Large-cap growth stocks have driven equity markets, and, more recently, those large-cap growth stocks have been seen as direct beneficiaries of the build-out of artificial intelligence capabilities.

Although we are not top-down macro-driven investors, we focus on monetary policy, economic growth, and inflation, meaning we do not attempt to time investments based upon such macro forecasts. However, macro factors most definitely impact the companies that we invest in and the bonds that we own; thus, we do pay attention to such factors, and as such, we develop base case assumptions to help inform us on sizing decisions of holdings within portfolios. Our base case assumptions provide insight into what holdings may be experiencing macro headwinds or tailwinds.

As we enter the last quarter of 2025, we are looking ahead to 2026. We maintain our base case of a continuation of guarded optimism around the economy, inflation, and corporate earnings. The guarded aspect of our base case boils down to how fragile the current goldilocks conditions appear to be. Broad inflation measures appear to be tolerated by markets near 3%. Still, we believe that any movement meaningfully above 3% will not be as well received and could put a chill on the optimism for further monetary policy easing. The same conditions are evident with economic growth and employment, where economic growth at an annualized rate between 2% and 2.50% does not stoke recession concerns. However, should that growth slip below 2% and if combined with an unemployment rate rising toward 5%, the complacency regarding recession worries would likely turn to a heightening of concern for both recession and lower corporate earnings.

As stated earlier, we do not invest around macro forecasting; however, our portfolios are not immune to changing macro factors. From a macro standpoint, we are expecting our portfolios to benefit from monetary policy easing overall, in contrast to how our portfolios reacted to monetary policy tightening in early 2022 and early 2023. In 2024, our portfolios generally performed well in response to the Federal Reserve embarking on rate cuts in the second half of last year, and we have already begun to see a similar positive reaction to the prospects of a resumption of rate cuts over the previous month. We welcome the resumption of the rate-cutting tail winds, and as always, our primary portfolio management focus remains on the fundamental factors related to our portfolio holdings.