Will Operation Epic Fury Cause an Epic Stock Market Correction? History Tells Us...

This seems like a good time to discuss the relationship between geopolitical risks/events and the stock market. In isolation, geopolitical risks/events have no direct relationship to the stock market. In fact, events that involve major military actions are inherently expensive and require the depletion of high-priced assets like missiles, drones, and combat aircraft when they inevitably get destroyed. This depletion leads to a demand for replacements, and this demand can move the needle on economic growth if the military action is more than a several-day targeted strike.

But of course, we all know that geopolitical risks/events can have second and third derivative effects, as we experienced following the Russian invasion of Ukraine in early 2022. This event, which is still ongoing, coincided with a market already beginning to price in higher inflation resulting from the reopening of economies around the world following the COVID-19 pandemic. The invasion itself directly disrupted grain and seed oil markets because Ukraine was a major global supplier of these commodities. However, it was the second-order effect of higher oil prices that resulted, not from the military action itself, but from the sanctions imposed on Russian oil exports.

The severe Bear Market in the equity markets in 2022 was not caused by the Russian invasion or even by the second-order effects, but one could certainly make the case that the invasion's timing made the Bear Market worse than it otherwise might have been.

When one has professionally managed investments for two or three decades and studied markets going back much longer than this, one comes to appreciate the psychology of markets and investors, and what such dynamics produce when market-moving situations arise. Wars are inherently unpredictable, disturbing, and unsettling to virtually anyone with a heartbeat. For investors, they must layer on very reactive markets that attempt to price in risks and hopes not just on a daily basis, but on an hour-to-hour basis, based on a constant flow of "expert" opinions, statements by politicians, and events on the battlefield.

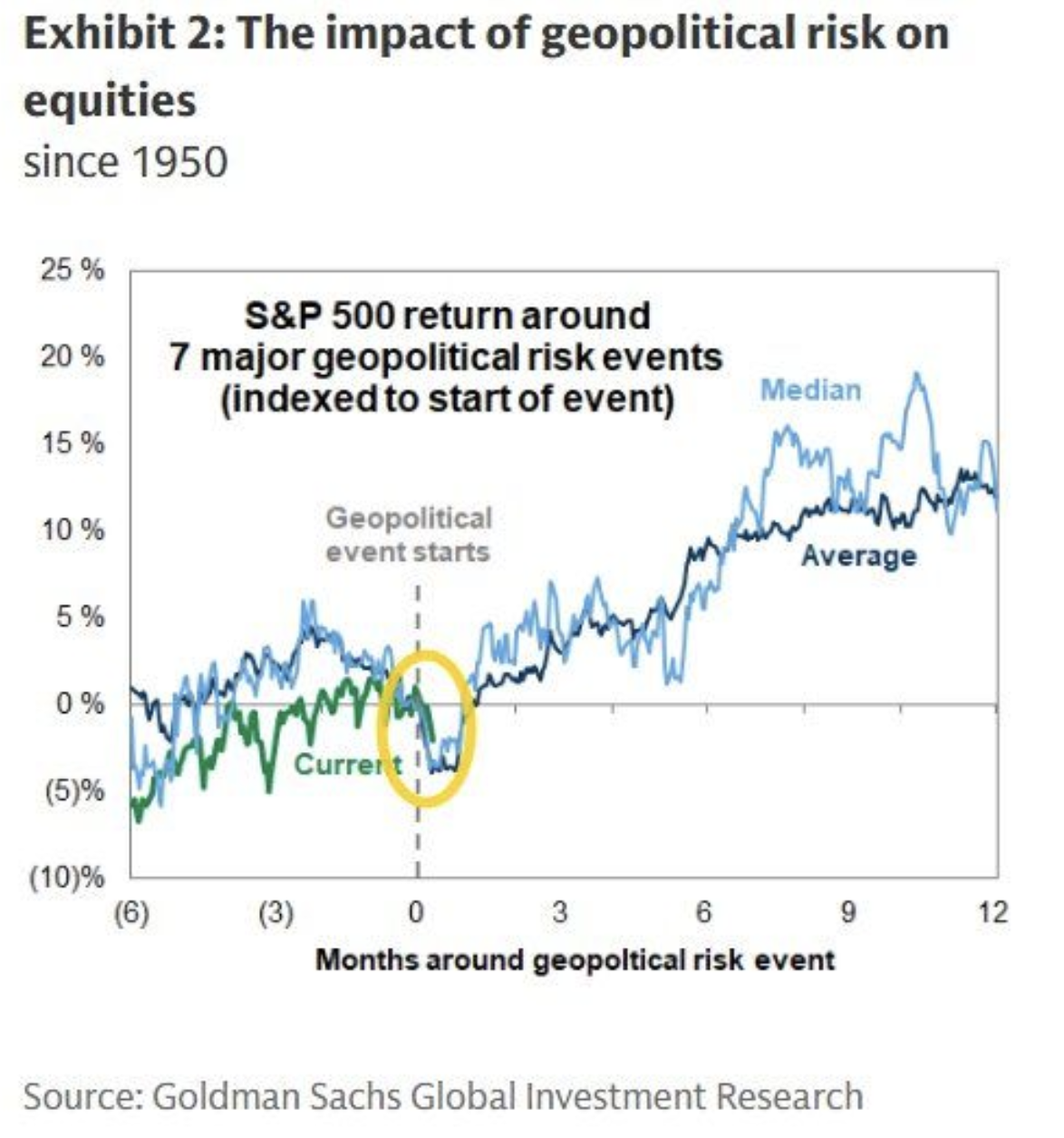

If we step back and look at market-moving geopolitical events over time, a pattern emerges. Goldman Sachs created the chart below recently, which charted the price action of the S&P 500 just before, during, and after major geopolitical events:

Based on the history shown in the chart above, investors should not panic-sell or become overly anxious about the impact of the current military action against Iran on their investments. As a professional investor, I take a mosaic approach based on an assessment of a continuum of risks. The military action against Iran by the United States and Israel falls within a continuum of risk assessment that became heightened following two events in the fall of 2024: the October 7th Hamas terrorist attack on Israel and Israel's resulting major military incursion into Gaza City, and the reelection of Donald Trump as President.

Both events, only a month apart, represented an inflection point on the market risk continuum. Since that inflection point, the equity markets, already fundamentally stretched from a valuation point of view, have had to attempt to price in a much higher level of geopolitical uncertainty and, as a result of the Trump Administration's abrupt reversal of 80 years of trade policy, a much higher level of economic uncertainty.

These mounting risks have resulted in the introduction of modest risk control measures in portfolios from the standpoint of asset allocation adjustments in balanced portfolios, the introduction of downside risk protection funds, and, more recently, the use of 1X inverse ETF products that rise in value equal to the drop in value of the underlying equity index. None of these actions are designed to significantly hedge against an unexpected 5-10% correction in the equity markets, but they are designed to calibrate equity risk in portfolios below what I would consider the baseline.

As I mentioned in the January commentary, I expect above-average economic growth for 2026, combined with below-average job creation. The equity markets will likely view such an environment as favorable for corporate earnings. If, on top of strong corporate earnings growth, we see further interest rate cuts from the Federal Reserve this year, we have a good chance of another above-average year in the equity markets. I consider any year that the S&P 500 is up over 10% an above-average year.

As we prepare to put the first quarter of 2026 behind us with a major war effort underway in the Middle East, oil prices near $100 a barrel for the first time since 2022, and a continuation of the tariff induced trade chaos, I see no reason to pull back on the risk control measures that we have put in place over the last 18 months. In fact, we are working to offer an options overlay strategy that should be available to many clients later this year, based on investment objectives and other suitability factors.

The type of options overlay strategy we anticipate being able to offer is designed as a conservative income solution in an environment of relatively low fixed-income yields and an S&P 500 dividend yield of barely 1%. Dividends paid by stocks used to be a material component of the long-term returns of equities, but over the last 15 years, that average yield has fallen 50%. One way to increase the income produced by a balanced stock-and-bond portfolio is to reduce the equity component and increase the bond component. In most cases, when an investor increases their fixed-income allocation to raise the portfolio's income yield, they will gain additional income but lose more in long-term capital appreciation.

For retirees, the flip side of longer life expectancy is a much longer time horizon for their investments. Assuming most people will tap into their retirement investment portfolios after they stop working, income becomes much more important in a retirement investment strategy. The falling dividend yield in the broad stock market has had unintended consequences for retirees seeking income to cover their voluntary withdrawals or the government-mandated Required Minimum Distributions (RMDs) from qualified retirement accounts. Many investors have either given up liquidity to earn higher income by using private debt funds or overweighted riskier interest-rate-sensitive investments such as Real Estate Investment Trusts (REITs) or leveraged bond funds and ETFs. With an "overlay" strategy, the associated investment account can continue to invest in a long-term growth-oriented strategy commensurate with the person's retirement time horizon, with the overlay designed to produce an additive, net-of-cost 4% or better income stream paid into the account.

I will have more to say about this over the coming months.